Welcome back.

Let’s join us

Reset password

Argentina's Turnaround: Could It Happen Elsewhere?

Heading 2

Paragraph

Heading 3

A rich text element can be used with static or dynamic content. For static content, just drop it into any page and begin editing. For dynamic content, add a rich text field to any collection and then connect a rich text element to that field in the settings panel. Voila!

Heading 4

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.

Heading 5

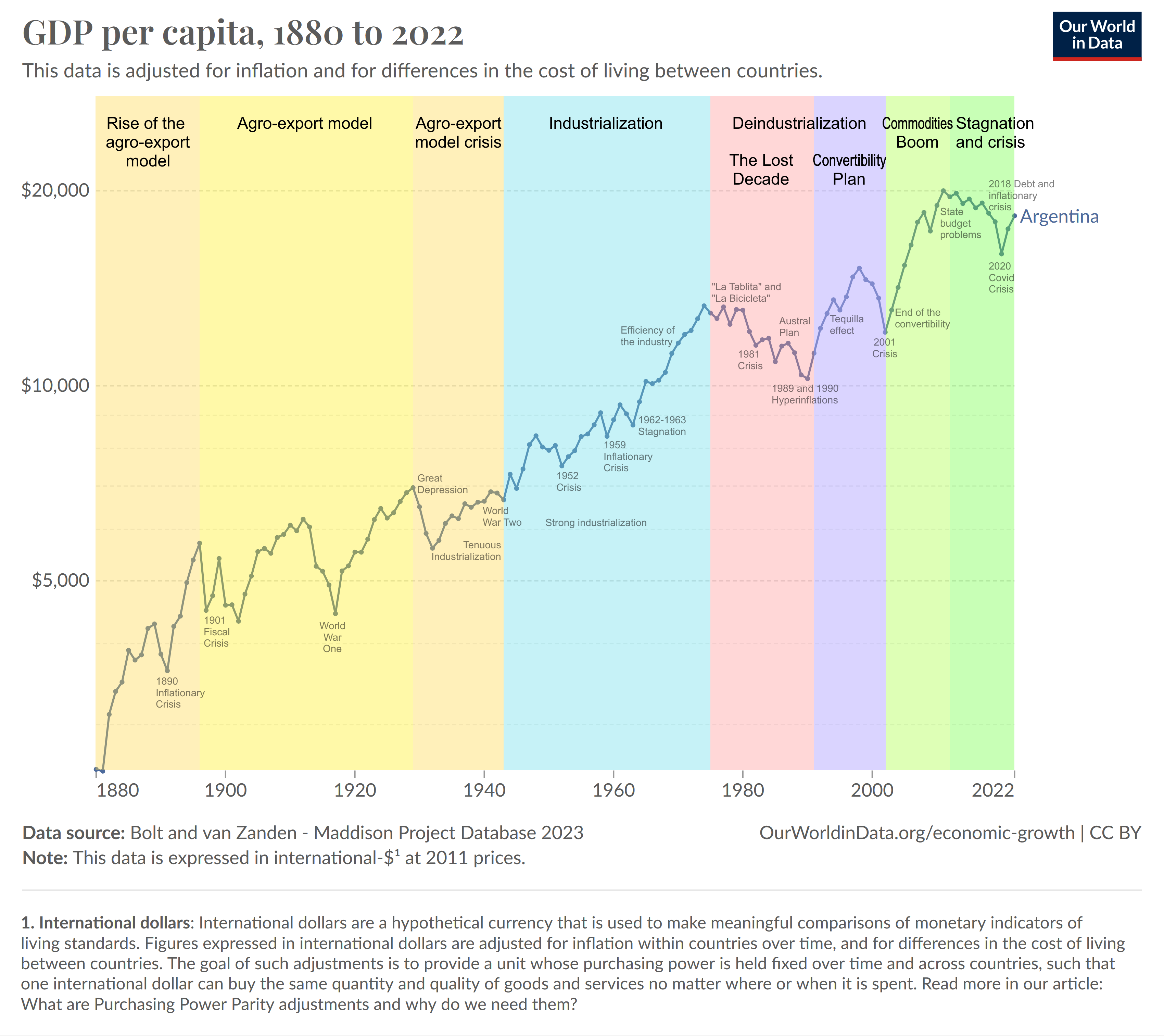

Even the most novice student of economics can tell you that historically, Argentina has had a very tough time.

Political volatility, austerity measures, and rampant inflation have led to high poverty rates, low foreign investment, and a large informal economy.

But lately, things are looking up. New president Javier Milei, an economist and self-described ‘anarcho-capitalist’, is quickly turning the situation around with his pro-market policies, spending cuts, and debt restructuring.

In this article, let’s take a look at how Argentina reached this point, how Milei is finding success, and what it means for the LATAM region going forward.

Argentina’s Economy: A Roller Coaster

Argentina’s modern struggles can be traced back to one man: Juan Perón. The controversial ex-president established his own political movement, Peronism, which has come to define the post-WWII era of politics and commerce in Argentina.

So what is Peronsim? Most political scientists classify Peronism as a left-wing populist movement. However, some have also tried to paint it as ultraconservative and even fascist.

The truth is that Peronism is sort of its own animal. A pro-worker movement that relied heavily on support from labor unions, Peron focused on reducing the wage gap, spurring development, and expanding worker’s rights and social protections.

And at first, it saw success. GDP per capita, industrial capacity, and exports all increased massively.

But, as with many political movements, the good intentions of Peronism gave way to failure, corruption, and poor decisionmaking.

The state-run industries that had once helped increase wages and fund social programs began to crack under the weight of mismanagement and the lack of competition. By the time Isabela Perón was forced from office in 1974, the country had entered a prolonged period of stagflation, which lasted until 1990.

Since then, the country has suffered bouts of hyperinflation, austerity measures, and exchange rate volatility. The country’s bond issuances have been slim, and its international credit is, in a word, poor.

There is a lot of historical nitpicking that could be done here, but the point is this: Argentina has been an economic problem child. Despite numerous attempts, it seems like the country just can’t get it together.

Enter Javier Milei.

Milei: The Renegade Capitalist

Fed up with a string of ineffective left-wing governments, the Argentine voters delivered Javier Milei a landslide electoral victory in November of 2023.

Milei is a widely-known economist and commentator who had previously held roles at HSBC, the Argentine government, and International Centre for Settlement of Investment Disputes. Popular for his anti-establishment, libertarian views, he vowed to root out corruption and mismanagement and restore prosperity to the country.

Now, over a year into his presidency, the results of Milei’s pro-market reforms are evident: equities and bonds have quadrupled in value in two years, and the country has posted fiscal surpluses for the first time in recent memory.

These shifts are rooted in pro-market reforms and increased trade openness, as well as a sharp fiscal adjustment and aggressive state downsizing policies. To date, Milei has re-privatized key state enterprises, devalued the Argentine peso by over 50%, and massively cut government spending.

The results have been impressive. The Argentine economy is expected to grow by 5.5% this year, coming off of decades of stagnant growth. The market response in recent years has been equally clear, with Argentine asset prices surging nearly 400%. Virtually all Argentine companies listed on the NYSE and Nasdaq experienced similar gains, regardless of sector—from banks like Banco Galicia (Nasdaq: GGAL) to agricultural firms such as Cresud (Nasdaq: CRESY). The Global X MSCI Argentina ETF surged from $34 to $93 between January 2023 and today.

These gains are not limited to financial assets—they extend to the local currency and physical assets such as farmland and real estate. In 2025, Argentina lifted its currency controls, leading to a roughly 10% appreciation of the peso and reinforcing market confidence. In the real estate sector, property prices rose by about 11% only in 2024, while rental yields remained around 5.5% annually in U.S. dollars.

This May marked the first political test of Javier Milei’s economic model, with elections held in some of the country’s most important districts, including the capital, Buenos Aires. The government’s victory in the legislative elections demonstrated—not only to Argentina but to the broader Latin American region—that it is possible to implement deep structural reforms while maintaining electoral support.

Argentinians so far seem to approve of this new approach. But will Milei’s model of trade liberalization, fiscal discipline, and aggressive spending cuts catch on in other LATAM countries?

Which LATAM country is next?

In 2026, two of the three most important countries in the region, Brazil and Colombia, will hold presidential elections. Both are currently governed by far left-wing leaders: Inácio Lula da Silva in Brazil and Gustavo Petro in Colombia. If there is a shift in the political landscape, asset prices in both countries could follow a trajectory similar to that of Argentina.

While both countries have significant potential, it is in Colombia where the need for change is particularly evident. This is reflected in President Gustavo Petro’s low approval ratings: his favorability ranks only slightly above that of leaders like Nicolás Maduro of Venezuela or Luis Arce of Bolivia.

Given the context, a shift in Colombia’s political winds appears increasingly likely, and financial asset prices have already begun to reflect this potential change. For instance, the Global X MSCI Colombia ETF has risen more than 25% year to date, while the Colombian peso has appreciated by 5.5% over the same period.

What could a pro-market leader accomplish for Colombia? Austerity and a reduction in government spending could help close the deficit, paving the way for better sovereign credit ratings and international credit. Lower deficits would increase investor confidence and help boost capital inflows.

A simplification and reduction of the tax burden would also be a welcome change. This would help attract FDI, make businesses more efficient, and enhance the competitiveness of exports. It would also help reduce the large informal labor market that exists in the country currently.

As we noted in last week’s article, there is a widespread mandate for meaningful change in Colombia, and the current frontrunners are all pro-market reformers. No matter who wins, we will likely see trade liberalization and increased foreign investment in Colombia. Although a 400% increase in asset prices does not seem likely, more effective leadership would certainly produce positive results.

Will the turnaround be as stark as Argentina’s? Probably not. Colombia hasn’t suffered the same fiscal woes that Argentina has, so there isn’t as far to climb. Nevertheless, the increase could be substantial.

What’s happening in Argentina is massively important. People are seeing, in real-time, that pro-market policies work. Don’t be surprised if a Milei-type leader emerges in Colombia or other LATAM countries - or if it has a huge effect on asset prices and economic performance.

Gain insider access to Farmfolio's network.

Receive weekly insights and updates directly from Farmfolio.